The battle between OLEDs and mini-LEDs

Liquid crystal displays with mini-LEDs are increasingly stealing a march on OLEDs, and micro-LEDs are already on the horizon, but production is complicated.

(Image: Ulrike Kuhlmann, c't)

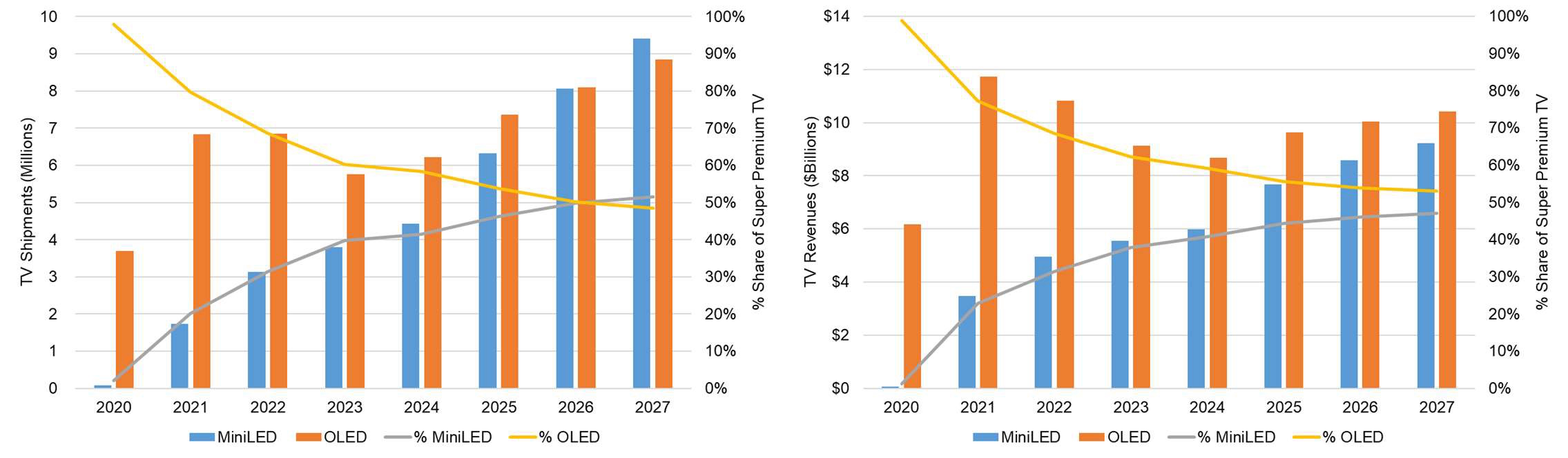

Two leading display technologies were put to the test at the Electronic Displays Conference in Nuremberg: OLEDs and LCDs with mini-LEDs in the backlight. While OLED stands for the highest quality and is therefore correspondingly more expensive, LED-LCD technology scores points with its enormous luminosity, rich colors, very high resolution and large diagonals, Bob O'Brien from the market research institute DSCC outlined the decision criteria that customers face when buying a television.

OLEDs are also currently available with 97-inch diagonals, i.e. almost 2.50 meters. However, only sets with so-called WOLED panels from LG Displays. Samsung currently supplies its organic displays called QD OLEDs with a maximum of 77 inches (1.95 meter diagonal). In Germany, QD OLEDs can only be found in smart TVs from Samsung and Sony; all other TV manufacturers use WOLED displays or LCD TVs with mini LED backlight. This year, Sony has even declared LCD TVs with mini-LEDs to be its high-end models and classified OLED TVs below them – this was not the case in previous years.

(Image: DSCC Advanced TV Shipment Report)

One reason could be the reduced production capacity for OLED panels, which O'Brien reported on, and the price differences: The high-color QD OLED panels with 4K resolution are significantly more expensive than comparable WOLEDs and even more expensive than mini-LED LCDs with four times the 8K resolution. As a result, the lesser-known brands or those looking for inexpensive devices such as Hisense, TCL, Skyworth or Toshiba tend to use mini LED LCDs rather than expensive OLED technology.

Videos by heise

They just want data

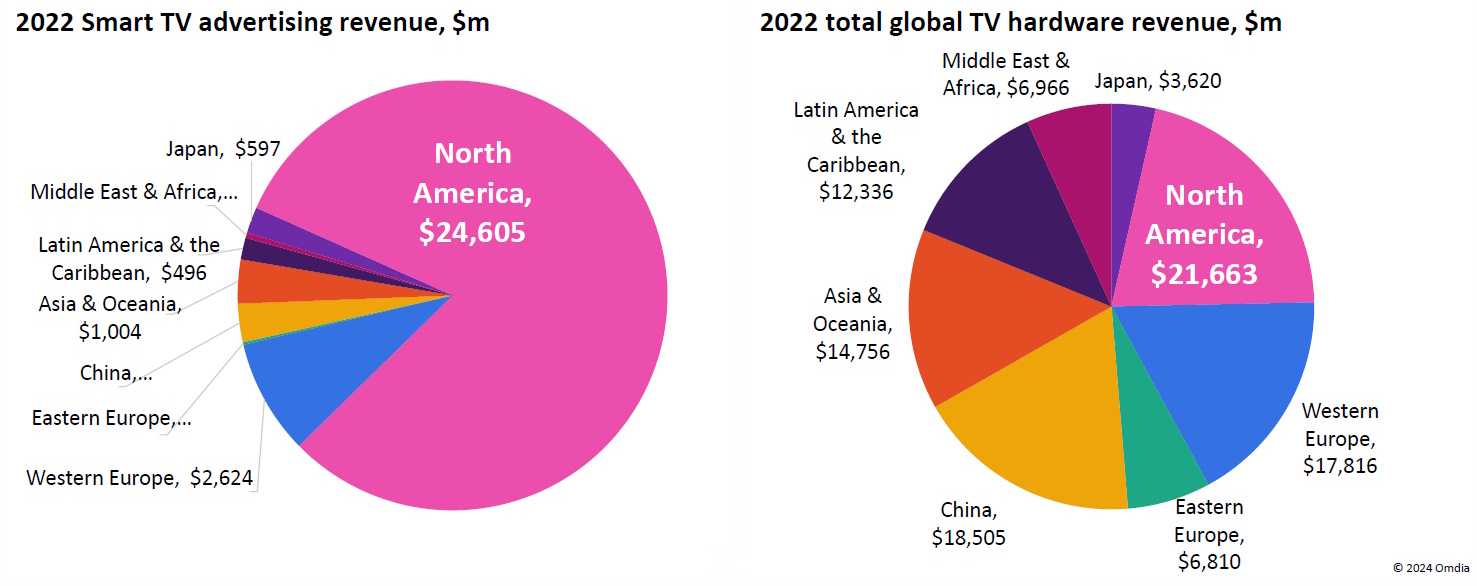

TV providers have developed a new business model during the pandemic in order to be less dependent on device sales. Or rather: they copied it, as YouTube has been pursuing the same strategy for years. It's all about ad-financed content, so-called FAST offers. Free ad-supported streaming is similar to linear television; you usually cannot fast-forward through the programs and are tied to the predefined program structure. As with traditional television, there is often a list of channels - and lots of advertising.

(Image: Omdia)

According to Paul Grey from the market research institute Omdia, TV manufacturers are already extremely successful with this in the USA. In this country, they still earn significantly more from the sale of smart TVs than from ad-financed apps.

However, if you look at the business model that Google pursues with YouTube, the acceptance of advertising is quite high. In the USA, Walmart therefore recently acquired the TV manufacturer Vizio. The company, which is only active in the USA, was an early adopter of FAST services for its TVs. In future, Walmart would like to use Walmart Connect to display advertising on its inexpensive entertainment devices.

(Image: Bob O’Brien, DSCC)

Pricing issues

At the height of the pandemic, flat screen sales skyrocketed and with them panel prices. This was followed by a crash two years ago. Prices rose again slightly in 2023 as manufacturers reduced their production capacities. The display industry is still recovering from the Covid boom, explained Bob O'Brien in Nuremberg. However, the chief analyst is not yet sure whether a trend is actually emerging here.

Samsung Displays (SDC) completely discontinued LCD production in 2022 and instead focused on organic displays, primarily for mobile devices. This made the Korean company more profitable than its domestic competitor LG Displays (LGD). Although LGD is still the leader in large OLED displays, the business is currently not particularly profitable.

Meanwhile, major competitor BOE is lurking in China, which in turn has significantly expanded its LCD production. BOE also has OLED fabs, but is still struggling with quality problems there - BOE is making slower progress than expected, particularly with large organic displays for TVs, despite substantial government subsidies.

(uk)